The growing demand for lithium, driven by the rapid expansion of electric vehicles and energy storage systems, has intensified interest in more sustainable and economically viable refining technologies that permit domestic refining capacity. Electrolysis-based lithium refining presents a promising alternative to conventional approaches, offering benefits in terms of reduced reagent consumption and effluent production, higher purity products and environmental footprint. This article provides an assessment of the current technological maturity and economic viability of electrolysis for the production of battery-grade lithium hydroxide. Economics are compared with conventional processing routes as well as other emerging technologies.

For more information on electrolysis-based lithium refining, please read the companion piece to this article, Electrolysis at Scale: Unlocking Sustainable Lithium Hydroxide Production.

Brine projects

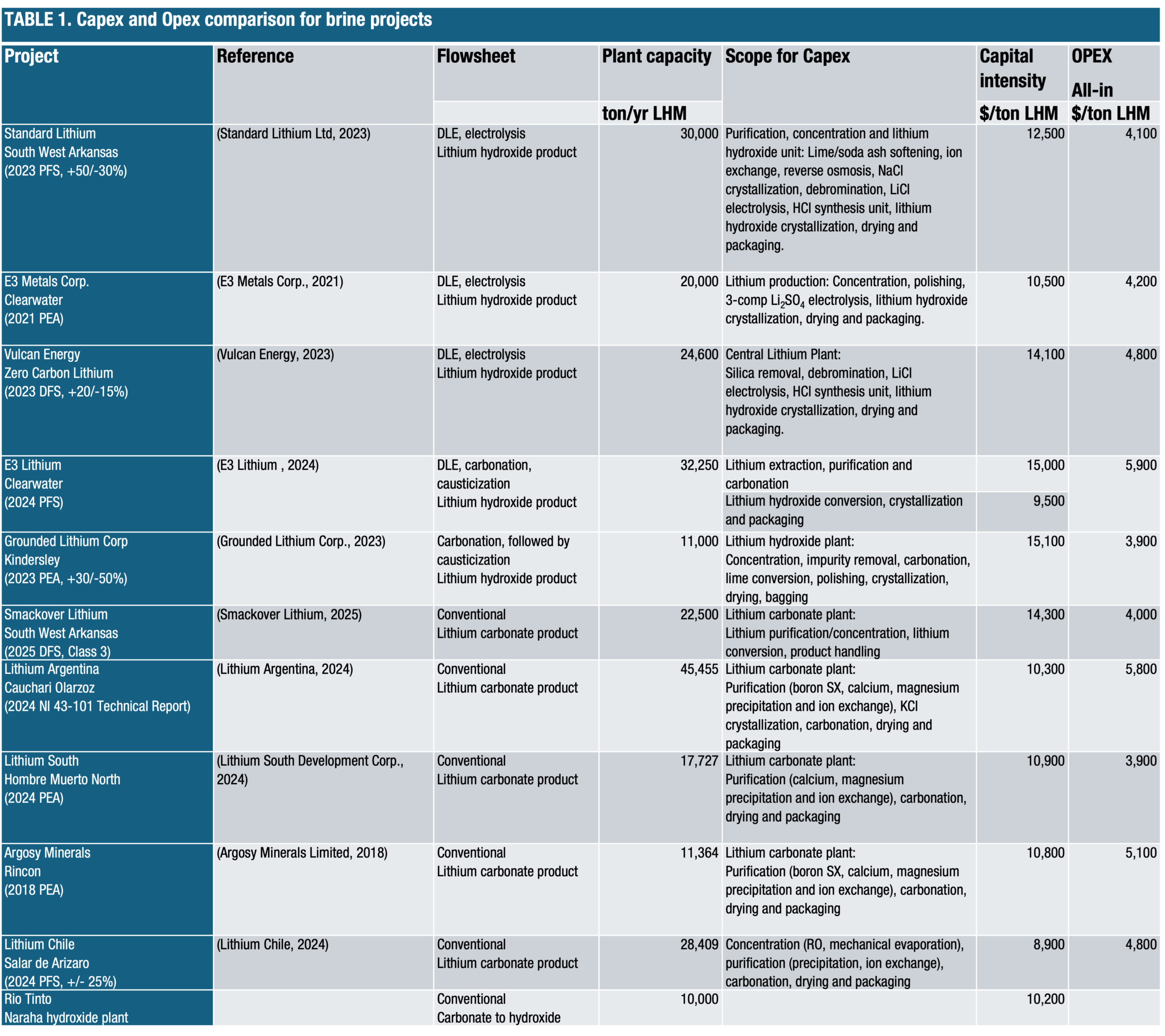

Capital and operating costs for a number of lithium brine projects are presented in Table 1. These figures are taken from published engineering studies, with the cost-estimate accuracy given where available and cost adjusted to a 2025 USD($) basis using Chemical Engineering Plant Cost Index (CEPCI).

The projects are split into three categories:

- Lithium hydroxide product via electrolysis

- Lithium hydroxide product via conventional carbonation and causticization

- Lithium carbonate product via conventional carbonation

Each project is accompanied by a brief summary outlining the scope associated with the reported capital expenditure (Capex) figures. To provide as close to like-for-like comparison as possible, the general scope for the projects takes a concentrated lithium brine and processes through to a battery grade lithium hydroxide or carbonate product. Capital intensity is reported on a lithium hydroxide monohydrate (LHM) basis, irrespective of the lithium product.

As the majority of the engineering studies considered do not break down operating cost by plant area, operating costs are presented as an all-in cost for the overall process, encompassing upstream extraction and direct lithium extraction (DLE) or solar evaporation operations.

Three projects utilizing electrolysis are evaluated, each accompanied by a brief summary outlining the scope associated with the reported Capex figures. In general, the scope encompasses key unit operations, such as impurity removal, electrolysis, hydrochloric acid synthesis (for projects using lithium chloride electrolysis), and the crystallization, drying and packaging of lithium hydroxide. Electrolysis demands an ultra-pure brine feed to extend the lifespan of membranes and anode coatings. Since brine compositions differ between resources, the specific pretreatment and impurity removal steps needed vary from one project to another. The average capital intensity across the selected projects is approximately $12,400 per ton of LHM. The average operating cost across the three projects is $4,300 per ton of LHM.

Only two engineering studies are considered that produce lithium hydroxide from brine via conventional causticization. As with the capex figures for the electrolysis projects, the scope for the Grounded Lithium Project numbers takes a post-DLE eluate solution and processes it through to battery-grade LHM; the capital intensity can be compared against the electrolysis figures to benchmark electrolysis against conventional processing. The capex breakdown in the Clearwater pre-feasibility study (PFS) does not allow a figure to be ascribed to a process taking a post-DLE eluate solution through to LHM. Instead, the processing plant is broken into two main plant areas for Capex purposes. The first comprises DLE, purification and carbonation and the second includes lithium hydroxide conversion, crystallization and packaging; the capital intensity of each plant area is $15,000/ton and $9,500/ton of LHM, respectively. Nonetheless, it is an interesting reference point for capital intensity associated with upgrading lithium carbonate to lithium hydroxide. It compares well with capital intensity for Rio Tinto’s Naraha facility (also included in Table 1), which converts a lithium carbonate feed from Rio Tinto’s Olaroz lithium plant in Northern Argentina into a battery-grade lithium hydroxide product via lime addition.

Capex and Opex figures are also presented for a number of brine projects producing a lithium carbonate product. If a similar capital intensity to the Clearwater and Naraha projects is applied to upgrade the carbonate to a hydroxide product, then direct conversion to hydroxide by electrolysis is, by comparison, a less Capex- and Opex-intensive process to a final hydroxide product.

Hard-rock projects

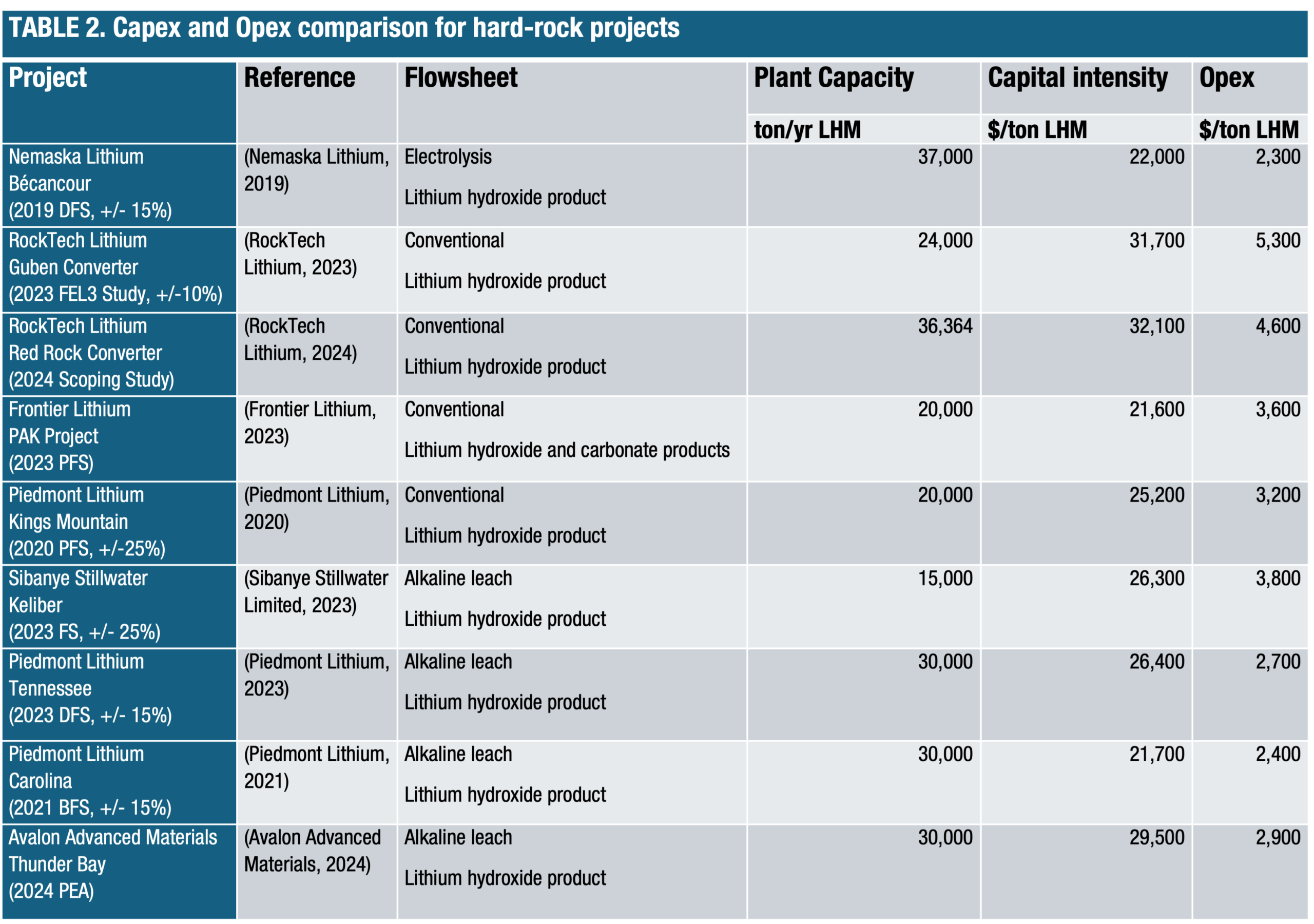

Table 2 presents a Capex and Opex comparison for a number of hard-rock lithium projects. Three processing technologies are considered, with the general flowsheet for each summarized below:

- Electrolysis: Calcination – acid roast – leaching – purification – electrolysis – crystallization

- Conventional: Calcination – acid roast – leaching – purification – causticization – crystallization

- Alkaline leach: Calcination – pressure leach – conversion leach – purification – crystallization

Projects have been selected that take a spodumene concentrate feed and produce a lithium hydroxide product. The basis for the Capex and Opex figures encompasses the full flowsheet from spodumene concentration through to LHM. Figures are taken from published engineering studies, with the cost estimate accuracy given where available and cost adjusted to a 2025 USD basis using Chemical Engineering Plant Cost Indices (CEPCI).

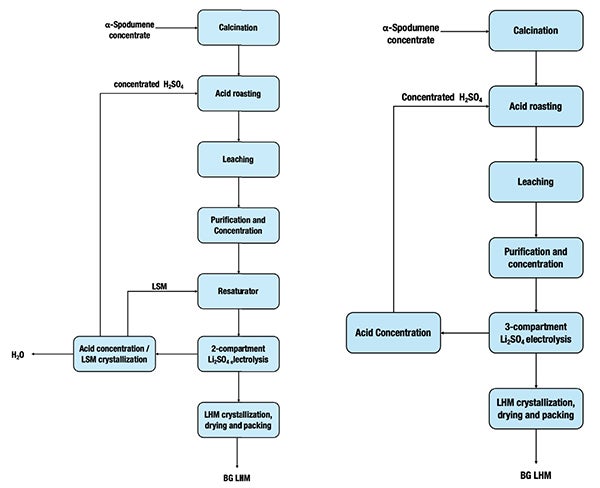

For electrolysis, the 2019 Pre-Feasibility Study for Nemaska Lithium (now majority owned by Rio Tinto) project is considered. This flowsheet adopted two-compartment lithium sulfate electrolysis and concentrates the anolyte acid product to recycle upstream to the acid roasting stage (similar to the general flowsheet shown here). While this is the only reference project for electrolysis, it should be noted that the study was completed to a +/- 15% cost accuracy.

{kind=link}

Across the selected projects, the average capital intensity for the electrolysis, conventional and alkaline leach flowsheets are $21,900, $27,600 and $25,900 per ton of LHM, respectively. The average operating costs for the three flowsheets are $2,200, $4,100 and $2,900 per ton LHM, respectively. Some of the projects evaluated provide a detailed breakdown of operating costs. One of the key observations is that reagent costs are significantly lower for the electrolysis flowsheet than for both conventional and alkaline leach processes.

- For the alkaline leach process, the main reagents are sodium carbonate and calcium hydroxide. Of the three projects including an Opex breakdown, the annual reagent costs were consistent at approx. $1,100/ton LHM and were the largest single contributor to operating costs.

- For the conventional flowsheet, the major reagents are sulfuric acid for the acid roast and leaching stages and sodium hydroxide for causticization. Annual reagent costs average approximately $1,600/ton LHM and were the largest single contributor to operating costs.

- While sulfuric acid is still required for the acid roast/leach stage, the electrolysis flowsheet benefits from recovery and recycling of acid generated in the electrolysis stage, reducing the amount of externally sourced sulfuric acid required. Incorporating electrolysis also eliminates the need for sodium hydroxide, with no reagent required for the electrochemical conversion of lithium sulfate to hydroxide. For the Nemaska project, reagent costs totalled only $200/ton LHM. The closed-loop nature of electrolysis flowsheets and reduced reagent consumption also reduces the carbon footprint associated with producing, transporting and handling large quantities of raw materials.

For the electrolysis flowsheet, the biggest component of operating cost is energy consumption, which contributes 20% to the overall Opex for the Nemaska project. Nearly 70% of this is associated with the electrolysis operation. Compared against the Piedmont Lithium Carolina project (alkaline leach), which assumes a similar unit power cost, the Nemaska project requires an additional $200/ton LHM in power costs. However, for this example, this additional cost is dwarfed by the reagent cost savings as shown above. Both of these projects benefit from relatively cheap energy costs.

Energy and reagent costs vary significantly across regions, which impacts how the competing technologies compare. The most attractive economics for electrolysis will be in regions with access to cheap, green energy and where reagent costs are expensive. ♦

Edited by Mary Page Bailey

References

- Argosy Minerals Limited. (2018). Argosy delivers exceptional PEA results for Rincon Lithium Project.

- Avalon Advanced Materials. (2024). Avalon Completes PEA: Post-Tax C$4.1 Billion NPV (8%) and 48% IRR at its Thunder Bay Lithium Processing Facility, ON.

- E3 Lithium . (2024). NI 43-101 Technical Report on Pre-Feasibility Study, Clearwater Project.

- E3 Metals Corp. (2021). NI 43-101 Technical Report Preliminary Economic Assessment Clearwater Lithium Project.

- Frontier Lithium. (2023). NI 43-101 Technical Report Pre-Feasibility Study for the PAK Project.

- Grounded Lithium Corp. (2023). NI 43-101 Technical Report: Preliminary Economic Assessment Kindersley Lithium Project – Phase 1 Update.

- Lithium Argentina. (2024). NI 43 – 101 Technical Report – Operational Technical Report at the Cauchari-Olaroz Salars, Jujuy Province, Argentina.

- Lithium Chile. (2024). NI 43-101 Technical Report and Pre-feasibility Study for Salar de Arizaro Project.

- Lithium South Development Corp. (2024). NI 43-101 Preliminary Economic Assessment Hombre Muerto North Lithium Project.

- Nemaska Lithium. (2019). NI 43-101 Technical Report Report on the Estimate to Complete for the Whabouchi Lithium Mine and Shawinigan Electrochemical Plant.

- Piedmont Lithium. (2020). Chemical plant PFS demonstrates exceptional economics and optionality of USA location.

- Piedmont Lithium. (2021). Piedmont completes bankable feasibility study of the Carolina Lithium project with positive results.

- Piedmont Lithium. (2023). Piedmont Lithium completes definitive feasibility study of Tennessee Lithium project.

- RockTech Lithium. (2023). Rock Tech Lithium Completes Final Engineering Study Before Construction of its Guben Lithium Converter.

- RockTech Lithium. (2024). Rock Tech completes Scoping Study for Canadian Lithium Converter.

- Sibanye Stillwater Limited. (2023). Technical Report Summary: Keliber Lithium Project, Finland.

- Smackover Lithium. (2025). Smackover Lithium Announces Positive Definitive Feasibility Study Results for its South West Arkansas Project.

- Standard Lithium Ltd. (2023). NI 43-101 Technical Report South West Arkansas Project. 6.

- Vulcan Energy. (2023). Vulcan Zero Carbon Lithium™ Project Phase One DFS results and Resources-Reserves update.

Authors

Clive Brereton is the chief technology officer of NORAM Electrolysis Systems Inc. (NESI; 12920 Mitchell Rd, Richmond, B.C. V6V 1M8, Canada; Email: cbrereton@nesi.tech). He is an experienced chemical process engineer with over 30 years developing new process technologies. He is also Vice President of NORAM Engineering and Constructors. Brereton has a Ph.D. in chemical engineering from the University of British Columbia and was a professor of chemical engineering at the University of British Columbia prior to joining NORAM in 1996. Clive is a Fellow of the Canadian Academy of Engineering, as well as a member of the UBC Chemical Engineering Hall of Fame.

Clive Brereton is the chief technology officer of NORAM Electrolysis Systems Inc. (NESI; 12920 Mitchell Rd, Richmond, B.C. V6V 1M8, Canada; Email: cbrereton@nesi.tech). He is an experienced chemical process engineer with over 30 years developing new process technologies. He is also Vice President of NORAM Engineering and Constructors. Brereton has a Ph.D. in chemical engineering from the University of British Columbia and was a professor of chemical engineering at the University of British Columbia prior to joining NORAM in 1996. Clive is a Fellow of the Canadian Academy of Engineering, as well as a member of the UBC Chemical Engineering Hall of Fame.

Jeremy Moulson is president and CEO of NORAM Electrolysis Systems Inc. (Email: jmoulson@nesi.tech). He is a Professional Mechanical Engineer with 14 years of experience in the electrochemical process industry with a focus on electrochemical technology development, scaleup, commercialization, and plant commissioning. Prior to the formation of NESI, Moulson was the business division manager of NORAM’s Electrochemical Technology Division. He has worked across the project and technology development space from early-stage concept development, prototyping and testing, mass manufacturing, project funding and financing and operational management of engineering teams and organizations. Moulson has a Master of Applied Science in mechanical engineering from the University of British Columbia.

Jeremy Moulson is president and CEO of NORAM Electrolysis Systems Inc. (Email: jmoulson@nesi.tech). He is a Professional Mechanical Engineer with 14 years of experience in the electrochemical process industry with a focus on electrochemical technology development, scaleup, commercialization, and plant commissioning. Prior to the formation of NESI, Moulson was the business division manager of NORAM’s Electrochemical Technology Division. He has worked across the project and technology development space from early-stage concept development, prototyping and testing, mass manufacturing, project funding and financing and operational management of engineering teams and organizations. Moulson has a Master of Applied Science in mechanical engineering from the University of British Columbia.

Luke Glynn (Email: lglynn@nesi.tech) is a seasoned process engineer with over a decade of experience spanning process design, development, scaleup, commissioning and plant operations, primarily within hydrometallurgical and electrochemical applications. Glynn has worked at NESI for over four years and currently serves as technical manager for Europe.

Luke Glynn (Email: lglynn@nesi.tech) is a seasoned process engineer with over a decade of experience spanning process design, development, scaleup, commissioning and plant operations, primarily within hydrometallurgical and electrochemical applications. Glynn has worked at NESI for over four years and currently serves as technical manager for Europe.